EVGA and NVIDIA To Split: EVGA Won’t Make Next-Gen NVIDIA Cards

by Ryan Smith on September 16, 2022 8:00 PM EST

In a move that will have significant repercussions for the video card industry in North America and Europe, EVGA today has announced that the company is parting ways from NVIDIA. As a result, the company will not be producing video cards based on NVIDIA’s next-generation of GPUs – and won’t be immediately switching allegiance to AMD or Intel, either. Consequently, NVIDIA is losing their largest add-in board (AIB) in North America, and the broader North American video card market is losing one of its biggest and best-known vendors.

In a brief announcement posted on EVGA’s forums, the company outlined their parting from NVIDIA, while underscoring that this affects the next-generation of video cards, and that EVGA will continue to provide current-gen products and support existing customers.

- EVGA will not carry the next generation graphics cards.

- EVGA will continue to support the existing current generation products.

- EVGA will continue to provide the current generation products.

EVGA is committed to our customers and will continue to offer sales and support on the current lineup. Also, EVGA would like to say thank you to our great community for the many years of support and enthusiasm for EVGA graphics cards.

EVGA Management

Meanwhile, in a briefing attended by Jon Peddie Research and Gamers Nexus, EVGA’s CEO (and founder) Andrew Han laid out some further details about the transition. These are both great pieces and as I’m not going to simply rehash them point by point, I’d encourage readers looking for a first-hand recounting of the briefing to check them out.

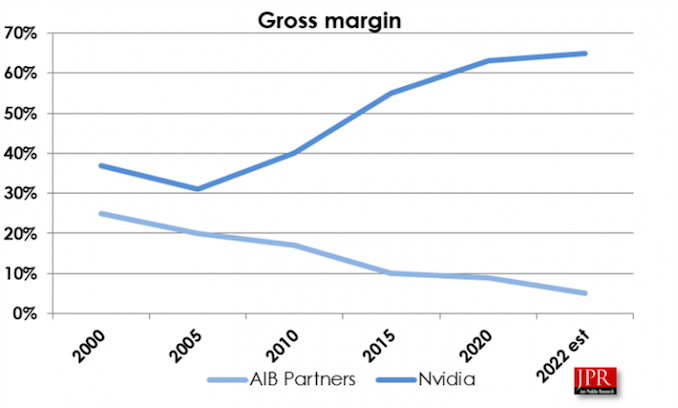

As laid out in both pieces, EVGA’s parting from NVIDIA comes as the company’s relationship with NVIDIA has, according to EVGA, soured over the years. Most notably, AIB margins have been slowly shrinking over the past couple of decades, with JPR publishing that gross margins at the AIB partners have fallen from 25% in 2000 to 10% in 2015, and finally an estimated 5% this year. Meanwhile, as NVIDIA has slowly ramped up its own efforts to directly sell its Founders Edition (reference) video cards in Best Buy and other retailers, AIBs like EVGA have been put in a position of directly competing with their partner-turned-supplier.

Jon Peddie Research: AIB Gross Margins v. NVIDIA Gross Margins

This, in turn, has put EVGA in a position where they are taking a loss on selling high-end NVIDIA cards, a significant shift from what are normally the highest margin products sold by video card vendors. And while consumers are benefitting from this in the short term via cheaper video cards, taking a loss of hundreds of dollars per video card is not sustainable – nor is it a viable business practice to begin with.

As a result of these factors (and undoubtedly more tales known only between EVGA and NVIDIA) EVGA has opted to part ways from NVIDIA. This means that EVGA will not be selling video cards based on NVIDIA’s next generation of GPUs, and that EVGA is ramping down production of existing GeForce RTX 30 series cards. According to Gamers Nexus, EVGA expects to run out of current-generation cards for retail by the end of the year, with the company setting aside a remainder of those cards as spares to honor warranty obligations.

EVGA RTX 3090 Ti FTW3: A Money-Losing Product

Perhaps equally notable, EVGA has also made it clear that they are not immediately partnering with a competing GPU vendor, either. So for the moment, at least, this is not going to be a case of EVGA switching allegiances to AMD or Intel. Instead, EVGA is going to be out of the video card market for an indefinite period of time. To be sure, according to GN and JPR, the company has not completely closed the door on partnering with another GPU vendor, but they also aren’t actively pursing the matter right now.

And while this marks a massive cut to EVGA’s business – Gamers Nexus reports that video cards represent 80% of EVGA’s revenue – EVGA is not going out of business. The company still has a successful and well-regarded power supply business, as well as a more niche presence in high-end motherboards and gaming peripherals. This also means that EVGA will continue supporting its existing video card customers even once their remaining video card stockpile runs out, as the company still wants to maintain its sterling reputation for customer service.

Commentary: A Big Loss for Consumers, and a Opening the Door To Vertical Integration

EVGA’s exit from the video card industry represents what is easily the biggest shift in the retail video card landscape in over a decade. EVGA is not the first NVIDIA partner to part ways with the company – BFG and XFX were both major NVIDIA partners back in the 00s as well – but EVGA’s exit would seem to be the biggest yet. According to JPR, EVGA held 40% of the North American retail market, and they were a sizable player in Europe as well. EVGA was NVIDIA’s de facto premiere partner in the west, both in terms of total video card volumes and in terms of mindshare, with a legacy of producing high quality video cards backed with some of the best support in the industry.

As a result, EVGA’s exit is a big loss for consumers and video card enthusiasts overall. While NVIDIA can (and undoubtedly will) shift allocations over to their remaining AIB partners – Zotac is arguably the next best-known NVIDIA-exclusive vendor in North America – this still represents a reduction in competition in video card designs, especially with premium products where EVGA did some of their best work. And none of the remaining AIBs have a reputation for support that matches EVGA’s (though to be sure, reputation isn’t necessarily representative of the real world).

EVGA's Immediate Future: More Mobos and PSUs

But the full impact to the consumer market is going to hinge on what NVIDIA does next. From EVGA’s briefing it’s clear that there has been some friction between the two companies for quite some time, so while these revelations are new to outsiders, internally the businesses have been at odds for a while now. That means NVIDIA had plenty of time to prepare for EVGA’s split (they were first informed in April), and NVIDIA already has their own retail operations.

In fact, it’s those retail operations that seem to have led the way to what’s happening today. It wasn’t until the Pascal generation/GTX 10 series (2016) that NVIDIA began selling its own retail cards; for the 20 years before that, NVIDIA relied on AIBs to move its products. And even after that point, NVIDIA has purposely limited its reach by only selling cards directly, and later just through Best Buy.

Still, I’ve long wondered how AIBs have felt about NVIDIA going into competition with their own board partners, and now we have an answer, it would seem. EVGA is being driven out in part by NVIDIA’s direct presence on the market, with their Founders Edition cards undercutting EVGA’s products in price. It’s a relationship that by its very nature puts AIBs like EVGA at a disadvantage, as NVIDIA has the better brand recognition (all cards are NVIIDA cards) and much of NVIDIA’s R&D is paid for by their internal need for reference cards. This means that AIBs face additional costs on top of buying hardware from NVIDIA, especially if they want to go for premium designs like EVGA has been apt to do.

In short, NVIDIA’s decision to directly sell video cards, whether intentional or not, is putting the squeeze on AIBs. And NVIDIA-exclusive AIBs like EVGA are the most vulnerable.

EVGA’s exit from the video card market, in turn, opens the door to larger changes in video card manufacturing and distribution. Video card complexity has increased significantly over the years, and consequently so have the R&D costs at every single level. GPUs aren’t just getting more advanced, but they need ever finer PCB routing for memory, more advanced VRMs, bulked up cooling, and more. It’s not unlike the fab market, where every generation ups the ante on costs and discourages the kind of competition that results in lower prices, lower margins, and the inability to afford to play in the next generation of the game.

All of this, in turn, is making vertical integration look more and more appealing. While the AIBs in one form or another have played pivotal roles in the video card market since the dawn of the PC era, offering retail reach and support that the GPU vendors didn’t have or didn’t want to bother with, the actual value they add is, unfortunately, diminishing. Video cards are becoming so complex that, especially at the high end, the best move may very well be to stick with the reference designs. All of which further reduces the value (and uniqueness) AIBs can provide.

EVGA's Experiments Haven't Always Panned Out...

In short, this may be the moment where we see video card production pivot to having the GPU vendors themselves sell their cards, without the use of AIBs. So rather than having 10 video cards within a generation and then numerous AIB variations thereof – as is the case now with NVIDIA’s GeForce RTX 30 series – we’d have something more akin to desktop CPUs where there’s a dozen or so SKUs provided directly by the manufacturer.

Of course, this has been tried once before, with disastrous results (kids, go ask your parents about 3dfx), so it’s not by any means a sure-fire thing. But EVGA’s departure opens the door to NVIDIA to swoop in and take back 40% of their retail market for themselves, if that’s what they want.

And if NVIDIA doesn’t fill in the gap, then NVIDIA’s remaining AIBs will no doubt be happy to do it. The volume vacuum from EVGA’s exit means almost half the NVDIIA North American video card market is up for grabs. It is a huge opportunity to reshape that landscape and grab the kind of market share that would take years and years to peel away under more normal circumstances. So although a dark day for EVGA, opportunity knocks for the AIBs who remain.

The next-biggest question at this point is whether EVGA will remain in the video card market at all. From the Gamers Nexus and JPR articles it’s clear that EVGA is not keen on immediately jumping back in with a different partner. And, given that the Ethereum Merge just went through this week and video cards across the globe were liberated from their inane toiling (read: Ethereum is no longer relying on proof-of-work for blockchain processing), now is not the time to be making any firm plans.

The broad expectations of the industry are that all of these former mining cards are going to be boomeranging back on to the used video card market, similar to the last crypto hangover but in even larger volumes due to the much longer period this most recent mining boom went on. So the video card market is going to be dealing with an oversupply as it is, meaning that it’s not going to be a great time to be producing more video cards, as even next-gen cards below the flagship level will be competing with their predecessors.

So even if EVGA does ultimately opt to get back in to video cards – and I hope they do – sitting things out while the market corrects itself and digests the sudden surge of used cards is a prudent move. How long all of that will take remains to be seen, but as the current situation took years to get into, it won’t be a fast fix coming back out. In time, it would be a feather in either AMD or Intel’s cap to line up EVGA as a partner, as they bring a level of sophistication and respect that none of their current AIBs possess. Though it should be noted that the overall GPU market share is so significantly tilted in NVIDIA’s favor right now – a 4:1 ratio – that at former production levels EVGA could probably absorb most of the AMD retail market presence, something AMD’s other AIBs would no doubt be unhappy with.

Unfortunately, this exit also underscores how exposed EVGA is in the video card market, since video card sales were 80% of its revenue. The company has other product lines, but these are smaller in volume and all in product categories that are even more commoditized than video cards.

Over the Years EVGA Has Gone Big Into PSUs, In More Ways Than One

EVGA, for its part, has certainly made efforts to diversify over the years, but with limited success. Almost a decade ago I was fortunate enough to be at a business dinner with EVGA and Anand, where Andrew Han asked for our feedback on what sorts of products we thought would be good markets for EVGA to expand into. We ended up making several suggestions, but as today’s EVGA product mix shows, EVGA never found a second market on the same order of magnitude as video cards. Consequently, I’m not surprised to see Gamers Nexus report that EVGA is not planning on expanding into new product categories in the near future; that’s not something they’ve had luck with in better times, never mind going into this likely recession.

Ultimately, while today’s news marks a seismic shift in the video card landscape, it’s also the kind of news where there’s no way to put a positive spin on it. The video card market, for its part, will keep moving right along without EVGA, but the market and consumers are all the worse for EVGA’s departure. Thankfully, this is not EVGA’s eulogy – the company is still staying in business – but I sincerely hope that when we talk about EVGA in the future, it will be for more than just motherboards and PSUs. Video cards are were EVGA has made its name, and it’s still where EVGA does some of its best work.

119 Comments

View All Comments

NickSam - Sunday, September 18, 2022 - link

The JPR gross margin chat is very misleading. NVIDIA have a big enterprise/data center business (AI, deep learning ...etc) that enjoys significant margins that resulted in their overall company 60+% gross margin. For AIB margin, another reference take a look at HK listed PC Partners (1263.HK), who owns ZOTAC, Inno3D and Manli - also have 80% of revenue from consumer graphics cards. Their latest (interim) 1H2022 finical reports list gross profit at 20.7% and net profit at 12.1% - I think that is representative of AIBs consumer graphics business.Bruzzone - Tuesday, September 20, 2022 - link

I agree JPR AIB gross margin take is many questions on the industrial management rules of profit maximization at every tier of the supply and sales distribution chain means Jon needs to replaced as Board Association Manager. mbBruzzone - Tuesday, September 20, 2022 - link

I'm not sure how many fell for less than profit maximization in the AIB supply chain but at x18 over the price of the GPU alone in 2021 everyone figured it out. Jon u'r fired. mb5j3rul3 - Monday, September 19, 2022 - link

The Historyiranterres - Monday, September 19, 2022 - link

"(though to be sure, reputation isn’t necessarily representative of the real world)."The article was decent until i've read this stupid line.

Bruzzone - Monday, September 19, 2022 - link

Data, situation assessment, questions and I trust some answers.Nvidia GA FE taper represents 17.4% of GA desktop PCI.

Nvidia GA mobile thrusts designed as Intel counter adds 26.6%

Nvidia Professional A series adds 6%.

Nvidia controls 50% of its supply.

I'm aware 3090ti FE entry price was meant to drag and press down inflated dGPU channel pricing on cartelization of the supply resulting in consumer discriminatory pricing between April 2021 and December 2021 that was up to x18 over the Nvidia price of the GPU component alone to the AIB.

Monopoly price premiums are x9 to x11 over the primary component price to the board house and at x18 is a cartel price. FE tapers were meant to lead price down but apparently interfered in AIB independent cost : price / margin decisions.

Here's a traditional cost : price / margin example industrially speaking on production economic best practice;

Risk production price = cost x2

Ramp if demand constrained usually not = cost x1.75

Peak production doubles volume now cost x1.5 = component price unless there is still a bunch of demand then the price will be held up. AMD and Intel are both basically x1.5 design producers.

Entering supply elastic price through run down = cost x1.25.

And at run end, the very last unit cost = price. This is what EVGA seems to have gotten got caught up in and EVGA walked.

NOTE while AMD and Nvidia RDNA ll and GA MSRPs at launch were fake PR prices, discriminatory to the board house, board houses made money all through 2021 on the basic cost : price / margin 'profit maximization' rule selling into national distribution. No one was losing money with end sales prices reaching x18 over the price of the GPU component itself to the AIB. Retail likely made the most money and that was AMD and Nvidia margin used to pay down the channels Intel inventory loss; cost : price offset.

Here are the AMD and Nvidia fake RDNA ll and Ampere prices

3080 @ $699

3070 @ $499

3060ti @ $399

3060 @ $319

6900XT @ $999

6800XT @ $649

6800 @ $580

Absolutely no way to make money at these suggested prices at x2.54 to x3.59 over the price of the GPU component alone to the AIB. x4 is considered the top end of a competitive profit but that only takes into account an OpEx 'variable cost' value. x5 enters economic profit point that begins to pay against R&D and int CapEx.

So, Nvidia said no or EVGA said no to forms of 'run end' cost : price / margin protection? This can include new product allocation discount to make up for prior losses and/or mobile inclusion and/or private label work or any number of mutually codependent business perks.

Was EVGA not only a board design producer but also Nvidia GPU broker dealer, reselling procurement overage to bring down the total cost of primary procurements? At run end means EVGA might have been caught with GA supply that was underwater in terms of brokerage.

I reported this on August 13 current card profit margin in the channel on sales price and that's all upstream from the sales outlet to the AIB [buffer] and then the component design producer. Notice much greater volumes of mid to bottom shelf is subsidizing top shelf.

3090ti makes 8% over cost

3090 losses 1.8%

3080ti makes 3%

3080 12 losses 13%

3080 10 price = cost

3070ti makes 10.4%

3070 makes 20%

3060ti makes 7.4%

3060 makes 16.2%

3050 makes 12% over cost

6950XT losses 4% over cost

6900XT loses 49%

6800XT losses 7%

6800 loses 14%

6750XT makes 25%

6700XT makes 10%

6650XT males 31%

6600XT makes 22%

6500XT loses 38%

6400 price = cost

Here's the volume to see how mid and bottom shelf on greater inventory volume is subsidizes the top shelf price discounting at retail.

AMD RDNA ll N6x desktop only

6950XT = 0.48%

6900XT = 9.30%

6800XT = 8.35%

6800 = 5.88%

6750XT = 0.79%

6700XT = 21.10%

6600XT = 16.93%

6650XT = 1.19%

6600 = 28.50%

6500XT = 5.76%

6400 = 1.71%

Nvidia Ampere RTX 3x00_ desktop only

3090ti = 2.26%

3090 = 13.99%

3080ti 12 GB = 7.70%

3080 12 GB = 13.83%

3080 10 GB = 10.76%

3070ti = 12.61%

3070 = 10.22%

3060ti = 10.76%

3060 = 15.07%

3050 = 2.79%

On AD, 4000 series are commercial and B2B cards foremost and AMD and Nvidia have been encouraged to price along a perfect pareto distribution curve, segment by segment application specific perfect pricing (on ROI) to prevent cartelization of supply and the channel running away with AMD and Nvidia margin that should be going to AMD and Nvidia. This method also protects AIBs insuring they also participate in profit maximization.

Here's my take on what AD price will be and if it's not I will quickly know why;

RTX 40x0 cost : price / margin assessment on GA real cost : price / margin on AIB x3 to x6 over their price of GPU itself that was not the fake MSRP.

I will also note x7 over cost of the GPU component itself is also not unreasonable for fully featured highest materials cards. And my down bin 'bottom shelf' here might be a bit low.

For engineers a bottom-up B.O.M assessment can be relied and I did that for TU and after a while just went with production economic multipliers over GPU cost to the AIB because it's an effective method that takes a lot less time. For example x5 would be the basic Intel CPU takes 20% of the PC price rule.

4090 = $2649 to $2931

4080ti = $1414 to $1545

4080 = 1146

4070ti = 877

4070 = 731

4060ti = 489

4060 = 441

4050 = 248

Ball parked but close enough on MC = MR entering AIB x3 to x6 over GPU price. I will know what any difference is and know what is and is not justified.

And here's past peak into run down price;

4090 = $1986

4080ti = $1060

4080 = 859

4070ti = 658

4070 = 548

4060ti = 439

4060 = 330

4050 = 186

Mike Bruzzone

Camp Marketing

Qasar - Tuesday, September 20, 2022 - link

blah blah blah blah blah blah blah ALL pointless and useless fluff, from the KING of Camp Fluff Marketing.probably mostly made up numbers. with NO links to sources for this, so no one can verify anything, its just BS. also sounds like he is drunk. come on Mike, stop posting this SPAM BS, unless you also post a SOURCE, and NO YOU are not a source.

Bruzzone - Tuesday, September 20, 2022 - link

'"probably" most made up numbers"', Quasar, I see you're beginning to come around, "probably", ,well good for you beginning to see the light!I offered and even posted formula's so anyone can figure this out on their own. Why aren't you Quasar doing your own assessments then we can have a back and forth on our determinations.

On my primary research the assessment is on channel, primarily ebay data, which you are aware.

On Nvidia AD price announced today 4090 at $1599 is a PR price let's see what the channel and AIBs price at. Ampere run end loss leaders, on GA inventory cost loss, will result in the channel setting premiums for Ada to make up their Ampere and other inventory losses for example Rocket S deadweight is a $4.5 billion industry and channel loss. Tiger U quad mobile also presents a huge surplus situation new inventory sitting on the shelf.

I will note that no one lost on Ampere throughout 2021 where card prices are as much as x18 over the Price of the GPU itself to the AIB. EVGA seems to have been caught holding inventory at run end where under profit maximization price falls to cost affects run end inventory especially if EVGA in addition to card design production is brokering individual GPUs to others as an Nvidia broker dealer.

I'm very close on 4080 between the two variants at an average of $1060 that is $11 more than the MSRP average but the weighted average will be different. One of the two cards 12 or 16 will sell in greater volume. Nvidia AD introduction price suggests NV is taking a 50% mark up over their cost / price from TSMC. I'll address this in greater detail as I have more data.

Some day Quasar please inform all how a primary source, primary research analyst is not the original source of their assessment. The data is channel primarily ebay and the calculations are basic production economic and profit max frameworks.

mb

Qasar - Wednesday, September 21, 2022 - link

" ,well good for you beginning to see the light! "nope all i see is a fraud and a fake.

" I offered and even posted formula's so anyone can figure this out on their own. Why aren't you Quasar doing your own assessments"

with what numbers Myke Brazzone ? the fake and made up ones that you pull out of thin air? what would the point of that be ? to prove you fake data is useful ?

" Some day Quasar please inform all how a primary source, primary research analyst is not the original source of their assessment. The data is channel primarily ebay and the calculations are basic production economic and profit max frameworks. "

the day you post links to your sources, will be the primary source, you are NOT a primary source, in any way shape OR form. as i said above, your just a fraud and a fake, who posts BS and fluff. you NEVER post a link to your sources, as there are NONE. every thing you post is BS, hell, a couple of people i have shown your posts to, asked me if you were drunk when you typed them, as some of what you type makes no sense and is just babble.

maybe change your name from, camp marketing to Camp Fluff marketing ? as that is what most of what you post looks to be, Fluff.

Dribble - Tuesday, September 20, 2022 - link

Most of the comments don't make sense - Nvidia is both making far too much money and screwing EVGA while undercutting them by selling founders cards cheaper.